|

Good afternoon. Corn and soybeans started lower in the overnight session Tuesday before buying again emerged after the 8:30am central reopen in soybean futures. Buying was not as prevalent in corn and wheat, which means funds have possibly gotten their positions squared for Friday. Fund positioning has been the name of the game early this week, while we are being told the US farmer has modestly rewarded the recent bump in board prices the last two days. Fundamentally, not a lot of change has been noted in recent days.

CN closed Tuesday at 4.67, down 2 cents. CZ was unchanged at 4.88 1/2. SN closed at 12.46 1/2, down 2 1/4. SX was up 8 1/4 at 12.28. WN closed at 67.42 3/4, down 6 cents. All five contracts made new highs for the week either last night or this morning. Products were mixed, July bean meal closed at 383.20, down $4.40/ton, and July bean oil closed at 44.50, up 66 points. Meal also made new highs. Livestock markets were higher, June live cattle closed at 177.62, up 65 cents, August feeders were up $1.55 at 254.42, and June hogs closed at 98.32, up 15 cents. Live cattle gapped higher to start this morning and closed near their lows for the day. Outside markets are mixed, both crude oil futures and stock index futures are trading either side of unchanged, and the US$ index is up 35 points.

Spreads were lower, corn spreads were around 1-2 cents weaker, while soybean spreads were down anywhere from a quarter cent to 10 and 1/2 cents. CK/CN closed at -13 1/4, and SK/SN closed at -14 1/4. Old/new crop spreads continue to trend higher in both corn and soybeans.

Cash sources are indicating farmer sales of both corn and soybeans have reached their biggest levels since the glut shot of harvest last Fall. Producers spent all Winter waiting for a South American weather rally, but one never came and they are now shedding bushels that have been in their bins for months. Sources say the South American farmer has also been a seller of soybeans on the recent rally. Bear spreading in Chicago futures has been noted on the increased cash movement. We've also noted a small back-off in basis bids, especially in the Western Corn Belt, which further lends credence to the idea that there was sizeable farmer selling in recent days.

Data on Tuesday included a StatsCan stocks report for Canadian grain/oilseed stocks as of March. The report showed stocks of wheat, corn and soybeans were all lower when compared to March of 2023, while Canola stocks were up y/y. Combined on farm and commercial wheat stocks were seen at 11,756 mt's, down from 13,901 mt's last year. On farm stocks went from 9,992 mt's to 8,403 mt's, while commercial stocks went from 3,910 mt's to 3,353 mt's. In corn, total combined stocks were seen at 8,263 mt's vs 7,033 mt's last year. On farm went from 5,699 mt's to 5,307 mt's, while commercial went from 3,376 mt's to 2,960 mt's. For soybeans, total combined stocks went from 2,064 mt's last year, to 2,046 mt's in 2024. On farm stocks were seen at 1,153 mt's vs 1,163 mt's, while commercial stocks were seen at 893 mt's, vs 901 mt's last year. And lastly for Canola, combined stocks were seen at 8,263 mt's vs 7,033 mt's last year. On farm was 6,689 mt's vs 5,750 mt's last year, and commercial stocks were 1,574 mt's vs 1,283 mt's last year. Other notable numbers included corn exports, which are quite small annually, being down 39% y/y, while soybean exports were seen up 15.3% y/y.

Energy and financial markets were mostly quiet today. Crude oil futures traded either side of unchanged despite increasing tensions in the Middle East. No ceasefire has been reached, and its being reported that IDF forces have taken the border crossing between Rafah and Egypt. It appears energy traders are growing numb to the daily headlines out of Gaza, as risk in the area remains heightened and the war efforts likely intensify in coming days.

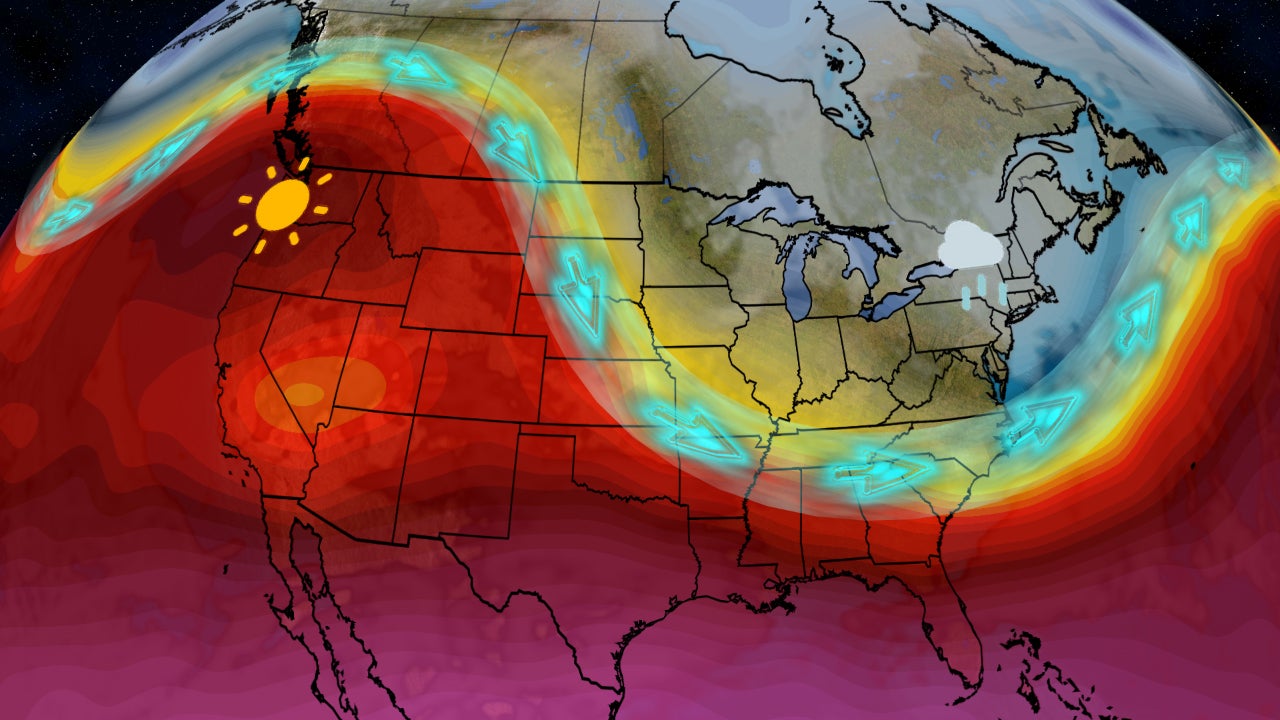

Weather forecasts are sticking with the same general pattern over the next week, while the exact precip amounts/locations are varying day to day. Three storm systems impact the Midwest today into the end of the week, with the heaviest rainfall totals favoring the Eastern Corn Belt. Confidence beyond 7 days remains low, but that the models have not changed off this pattern for several days is a good development. Both the EU and the GFS also both see increased rainfall chances for Western Kansas in the next week, also a positive development. Temps will begin warming in the West starting Thursday and look to remain above average into next week, while the East will be slightly cooler than average.

For South America, it appears there was a data delivery error in this morning's EU model update, as the forecast has returned moisture to far Southern Brazil, and also brought back the temp forecast from the end of last week. Argentina sees frost potential over the next 10 days for most of the country, with cool temps even stretching into some parts of Southern Brazil. Heat is seen subsiding in most of Central Brazil in the next 10 days as well. Debate remains as to soy crop loss due to flooding, with estimates generally in the 1.5-2 mmt ballpark. The death toll from the flooding has now reached 90, and is likely not done increasing as the floodwaters have only just begun retreating.

|

.jpg)